There has been much debate in the autism community whether “awareness” is still a worthwhile goal. I very much believe that, no matter how tiresome, frustrating, or potentially divisive, these debates are important. They do a lot to help shape my ever-changing feelings about autism, help guide my parenting decisions, offer me new resources for ideas, and aid me in attempting to see the world as my child does.

Another thing I very much believe: Awareness remains a worthwhile goal. It’s not the only goal, of course, but we have a long way to go as a society towards understanding the differences of not just those with autism, but all types of people. I know that being a parent of a child on the spectrum has altered — to a great degree — how I view other people, particularly those that don’t seem to fit the mold. It was a forced, and very valuable, lesson in awareness.

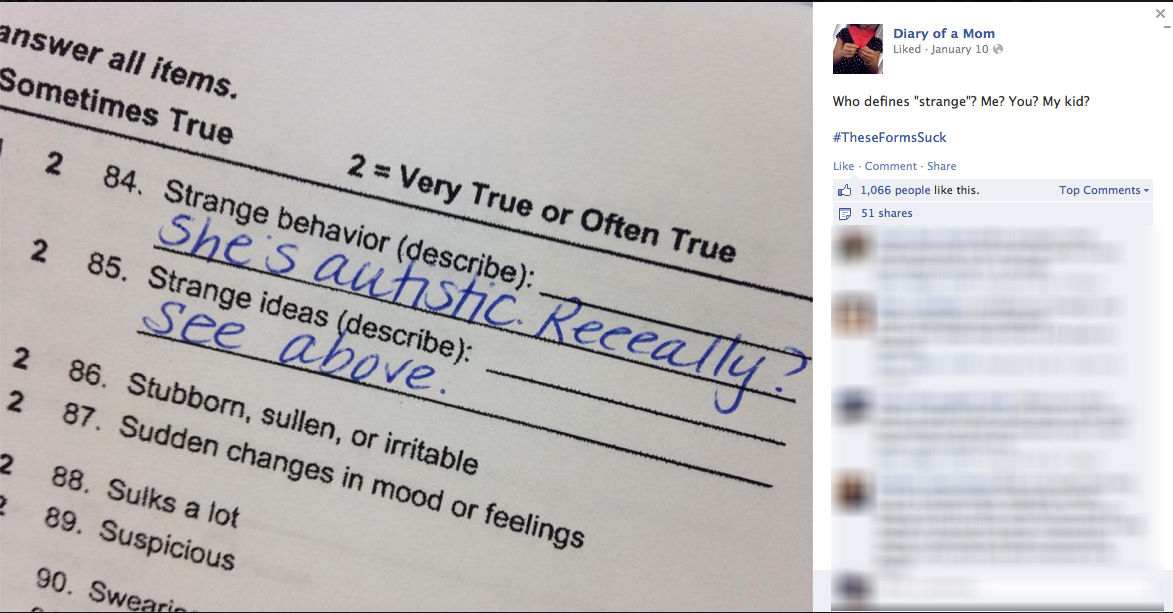

One need look no further than standardized forms to realize that awareness has a long way to go. Jess from Diary of a Mom posted the following on her blog’s Facebook page the last week, but I think all parents of special-needs kids probably have some similar experience:

A: Yes. Yes it does.

It was some sort of behavioral assessment form that called for the parent to list the child’s “strange” behaviors. Jess replied with, “She’s autistic. Reeally?” On Facebook, she added:

Who defines “strange”? Me? You? My kid? #TheseFormsSuck

The question, and her response, jogged for me a memory of a rather unpleasant experience. A few months back, after a standard financial review, Veronica and I decided to buy additional life insurance. I turned to the company we use for all our financial needs, one whose sterling reputation for customer service is well deserved and has driven me to give it more and more of my business.

The policy we intended to buy included a complementary rider to cover our kids. For free, it sounded like a good idea. Veronica and I scheduled, and underwent, standard medical exams for our policies without issue. The next step was a phone interview about our kids’ general health — standard operating procedure before a policy could be issued.

Everything was fine until I began answering questions about Ryan. He has seen a psychiatrist and psychologist and taken medication for anxiety. I explained that he was on the autism spectrum and anxiety was a common co-condition.

That’s when things got ridiculous. Reading from a standard form, the interviewer asked me, “when was the last episode of the autism?”

I’m pretty sure I laughed out loud. I knew she was simply reading a script but I was still amazed. Autism is not the flu, I told her. It’s a life-long developmental condition. He does not have “episodes” of autism. He has autism. Period.

She pressed. The form could not be completed without an answer to the most recent occurrence. So I told her to put “ongoing” or something similar and she promised to put a note at the end of the form explaining that the question didn’t make sense.

I was miffed, but we managed to get through the interview and I was told I’d hear back after the policies were reviewed.

A few weeks later we got the response: Riley’s policy could be issued, but they were rejecting coverage for Ryan, we were told, because of “the autism.”

I inquired what that had to do with life expectancy and was told it had been flagged by their underwriters and they had no choice. I asked for a follow-up call, which I received. The person who contacted me told me that because of the higher possibility of depression, they could not issue a policy covering Ryan. She didn’t have to say any more.

To be honest, the refusal to issue a free rider on our policy wasn’t what upset me. I understand insurance is a business that is all about evaluating risks and estimating potential costs. The company has to conduct thorough reviews about the policies it issues. I get that by being truthful in my answers, Ryan’s risk factors scored above an acceptable range for issuing such a policy. I’m sure that if I really needed life insurance for my middle-school age son, I could do so, albeit at an elevated cost. Again, I get it. It’s a formula. If the insurer believes there are factors, be it depression or tobacco use or high blood pressure, that increase the likelihood of a policy being paid out, they have to evaluate that information carefully and make a decision.

What upset me was the absurd nature of the questions upon which this decision was made. I decided that since I already had someone from the insurer on the phone, I would at least make them aware of how I felt.

I inquired how their questions could be so out of touch about a diagnosis that has become incredibly common. I asked how they expected to continue to do business if they were going to automatically eliminate so many potential customers based on a complete lack of understanding of a neurological condition. I advised them that they really needed to revise their questions. I asked for someone to follow up.

No one did.

So they did not get my business. The policies that were completely written and ready for Veronica and myself (and Riley) went unsigned.

I think of this episode when the worthiness of “awareness” is debated. Clearly, we have a way to go.

I have bristled at some “standard” questions, too. The insurance companies DO need.to update their materials. It is way past due. Great post!

LikeLike